|

|

PNB Branches

Facilitation Services |

Products and Services |

Home Loan |

Global Directory |

About Us |

|

Stay up to date with the latest events and announcements from Philippine National Bank. |

TEMPORARY CHANGE IN BANKING SCHEDULE

To our Valued Clients,

In the interest of public health and safety, PNB Los Angeles Branch will temporarily suspend operations during Saturdays effective March 21, 2020 until further notice.

We are still OPEN Monday to Friday from 9am-3pm to serve your banking needs.

Thank you for your continued patronage.

INCREASE IN SERVICE FEES FOR US DIRECT DEPOSIT ACCOUNTS

Dear Valued Client,

Please be advised of the increase of service charge for the crediting of monthly pensions for all PNB DIRECT DEPOSIT PESO Accounts as follows:

| FROM | TO |

|---|---|

| $7.00 | $8.00 |

Note: Service charge for PNB Direct Deposit US Dollar Account remains the same at $10.00.

New charges take effect January 2, 2020.

Thank you.

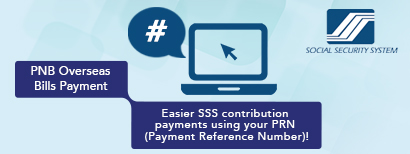

SSS CONTRIBUTION PAYMENTS

To our Valued Clients,

Enjoy real-time posting of your contributions to your SSS records. Simply present a valid PRN (payment reference number) when making contribution payments.

Please visit www.pnb.com.ph/obps-sss for more information on the SSS payment process.

Thank you.

RELOCATION ANNOUNCEMENT

In line with the continuing thrust of PHILIPPINE NATIONAL BANK to serve its customers better, effective April 29, 2019, PNB LOS ANGELES BRANCH have moved to 3435 Wilshire Blvd., Ste 104 Los Angeles, CA 90010.

Thank you.

| HOME | PRODUCTS AND SERVICES | HOME LOAN | DIRECT DEPOSIT | CONTACT US | 3435 Wilshire Blvd. Ste 104 Los Angeles Ca 90010 |